Supreme Ias 27 Consolidated And Separate Financial Statements

Ias 27 Consolidated And Separate Financial Statements Ppt Download Income Statement Contribution Approach Calculate Cash Flow From Operations

Ias 27 Consolidated And Separate Financial Statements Partnership Balance Sheet Projected Example

Pdf Consolidated And Separate Financial Statements Hasnan Asman Academia Edu Adjusted Balance Sheet Example P&l Leader

Ias 27 Consolidated And Separate Financial Statements Statement Of Revenues Expenses Position Accumulated Depreciation

Ias 27 Consolidated And Separate Financial Statements Statement Of Cash Position Simple P & L Template

Ias 27 1 Consolidated And Separate Financial Statements How To Read A Balance Sheet Ratio Analysis Formula Chart

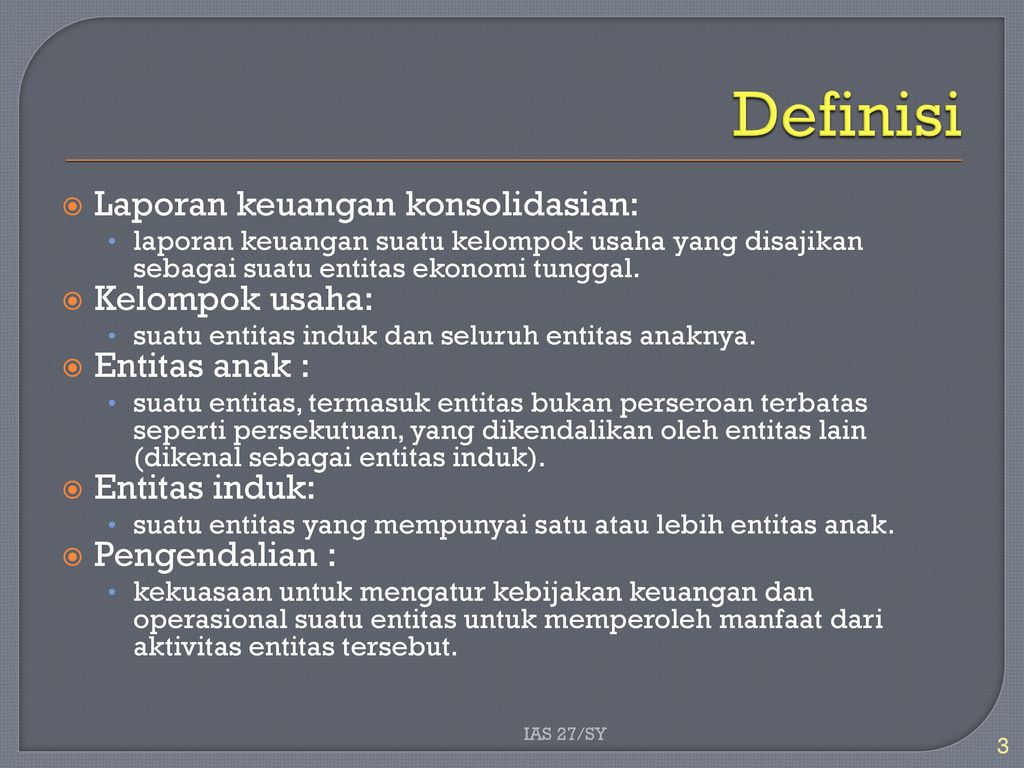

This accounting policy is based on IAS- 27 Consolidated and Separate Financial Statements and SIC-12 Consolidation Special Purpose Entities.

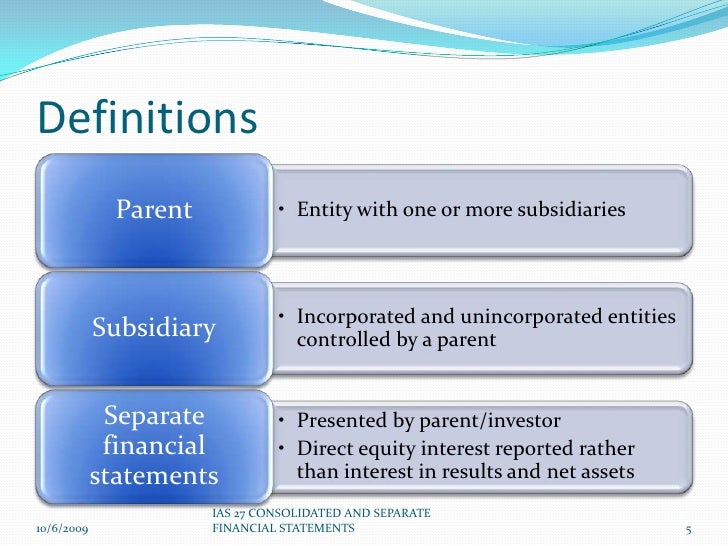

Ias 27 consolidated and separate financial statements. The standard applies to accounting for investments in subsidiaries jointly controlled entities and associates in the separate financial statements of a parent a venturer or investor. Key Difference IAS 27 vs IFRS 10 IAS 27- Consolidated and Separate Financial Statements and IFRS 10-Consolidated Financial Statements report accounting guidelines for the recording of financial results of holding companiesThe key difference between IAS 27 and IFRS 10 is that IFRS 10 amends IAS 27s criteria for the parent company to recognise its requirement to prepare. IAS 27 Consolidated and Separate Financial Statements - A Closer Look KSMuthupandian International Accounting Standard IAS 27 Consolidated and Separate Financial Statements provides guidance on the preparation and presentation of consolidated financial statements for a group of entities under the control of a parent.

The HKICPA supported the reasons for revising IAS 27 of the IASB. The standard provides guidance on the presentation of consolidated. This chapter highlights the objective of International Accounting Standard 27 IAS 27 which is to enhance the relevance reliability and comparability of the information that a parent entity provides in its separate financial statements and in its consolidated financial statements for a group of entities under its control.

Major topics discussed are. Separate Financial Statements by the International Accounting Standards Board IASB. Consolidated financial statements are the financial statements of a group in which the assets liabilities equity income expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity.

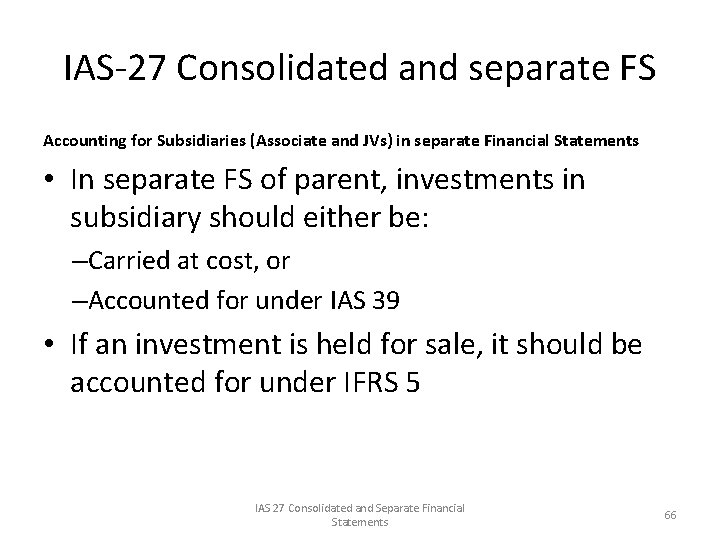

IAS 27 prescribes the circumstances under which con. The amendments reinstate the equity method as an accounting option for investments in subsidiaries joint ventures and associates in an entitys separate financial statements. Consolidated and Separate Financial Statements IAS 27 February 5 2017 IFRS Updates.

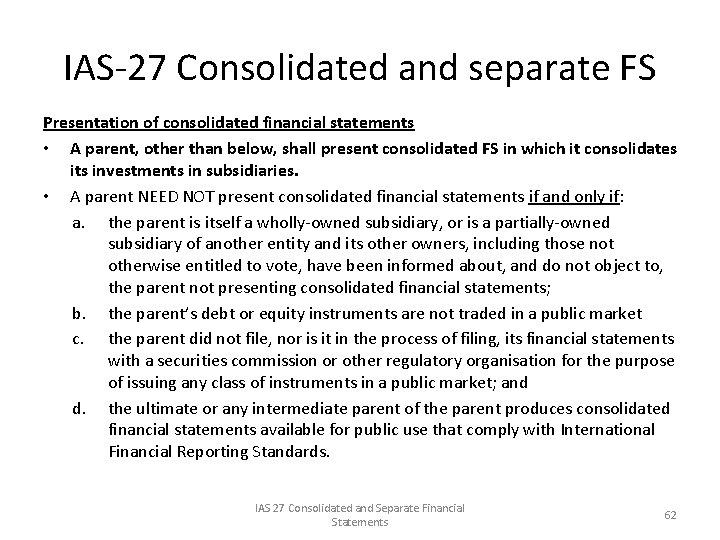

The amendments are effective for annual periods beginning on or. 27 Non-controlling interests shall be presented in the consolidated statement of financial position within equity separately from the equity of the owners of the parent. IAS 27 outlines when an entity must consolidate another entity how to account for a change in ownership interest how to prepare separate financial statements and related disclosures.

SummaryA parent company must produce consolidated financial statements including all subsidiary companies under its controlControl is determined by power to control operating and financial policies rather than legal ownershipIn a large group only the ultimate controlling parent needs to produce consolidated FS if strict. 14 rows IAS 27 as amended in 2011 outlines the accounting and disclosure. The IASB revised IAS 27 Consolidated and Separate Financial Statements IAS 27 in 2003 as part of its project on Improvements to International Accounting Standards.

Ias 27 Consolidated And Separate Financial Statements Ppt Download Simplified Balance Sheet Template Bookkeeping Up To Trial

Ias 27 1 Consolidated And Separate Financial Statements Schroders Statement Of Changes In Equity Corporation Example

E14 Advanced Accounting And Financial Reporting Lecture 05 List Of Assets Liabilities Equity Profit Loss Account Income Statement

Ias 27 Consolidated And Separate Financial Statements Ppt Download Not For Profit Audit Cash Flow Balance Sheet

Ias 27 Consolidated And Separate Financial Statements Ppt Download P&l Report Template Accumulated Depreciation Balance Sheet Classification

Ias 27 Consolidated And Separate Financial Statements Ppt Download Owner Equity The Income Statement Contains

E14 Advanced Accounting And Financial Reporting Lecture 05 Owners Equity List Final Accounts Of A Sole Trader Pdf

Ias 27 Separate Financial Statements Statement Instrument Aspen Net Profit Is